ITAT Restores Section 11 Exemption Claim, Directs Fresh Examination After Late Form 10B Filing

ITAT Restores Section 11 Exemption Claim, Directs Fresh Examination After Late Form 10B Filing

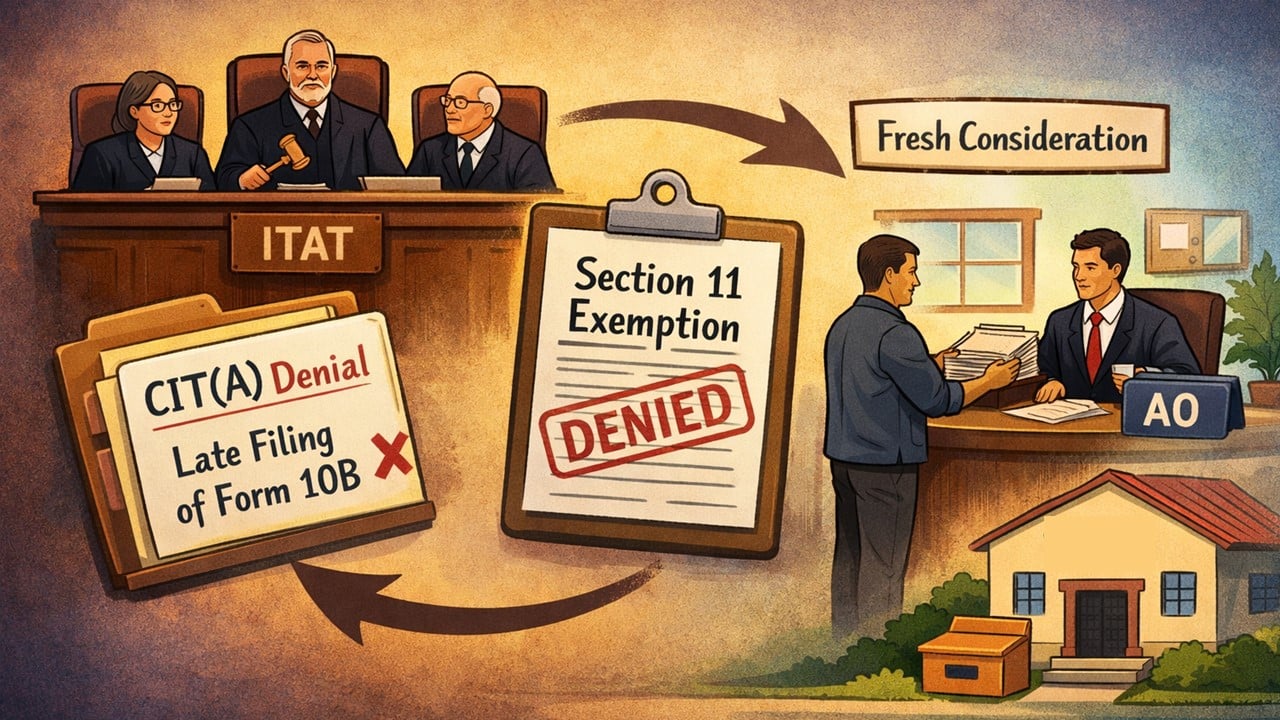

ITAT Panaji sets aside CIT(A)’s order denying Section 11 exemption due to late Form 10B, sends the case back to the AO for fresh consideration after deciding the pending delay-condonation application and granting proper hearing to the assessee.

The present appeal has been filed by the Dearhood Foundation in the ITAT Panaji, challenging an order passed by the CIT(A) denying the assessee’s claim of exemption under Section 11 of the Act. The case is related to the Assessment Year 2022-23.

The assessee is set up under Section 8 of the Companies Act 2013 and is registered under Section 12A(1) of the Income Tax Act. The assessee filed its income tax return (ITR) using ITR-7 for the year in consideration, declaring total taxable income as ‘NIL’ after availing exemption under Section 11 of the Act. During processing of the return, the Assessing Officer (AO) assessed the total income of the assessee at Rs. 14,62,003 by disallowing the claim of exemption under Section 11 of the Act on the grounds that the assessee did not furnish Form No. 10B and the CPC has raised a tax demand amounting to Rs. 5,33,910.

The aggrieved assessee filed an appeal before CIT(A). The CIT(A) noted that the assessee has claimed exemption under section 11 of the Act. On the other hand, Form 10B was furnished late, after the statutory extended due date as per CBDT Circular no. 20. The form was submitted almost 10 days ago. The CIT(A) also noted that the assessee had urged for condonation of delay in filing Form No. 10B before CIT(E) Bengaluru, but could not furnish relevant evidence explaining the reason, and the same is pending to date. Finally, concluded that the assessee is not entitled to enjoy the exemption under Section 11 of the Act and dismissed the appeal.

Thereafter, the assessee filed an appeal before the ITAT Panaji challenging the aforesaid CIT(A)’s order. When the tribunal analysed the case and verified the facts of the case, it noted that the assessee had applied for condonation of delay before CIT(E) Bengaluru, and the case is still pending for disposal. Considering the CIT(A)’s findings and principles of natural justice, the tribunal noted that the assessee had not been provided a proper chance of hearing yet; hence, it set aside the CIT(A)’s order in question and remanded the case back to the AO for fresh consideration.

The AO has been directed to first look at the result of the delay-condonation application filed by the assessee before the CCIT(E). After that, examine the assessee’s claim for exemption under Section 11 of the Act. Make sure the assessee is being given a proper opportunity of hearing. The assessee has also been directed to fully cooperate with tax authorities by submitting all necessary information. Accordingly, the assessee’s appeal was allowed for statistical purposes.